Reasons Not to Invest in Principal LifeTime Target-Date Funds…

Reasons Not to Invest in Principal LifeTime Target-Date Funds…

In 2014, American Chemicals & Equipment, Inc.(ACE) 401(k) Retirement Plan filed a $300 million lawsuit against Principal Management Corporation and Principal Global Investors, llc, Civil Action 2:13-cv-1601-AKK, in the U.S. District Court, Northern District of Alabama. The action was filed on behalf of the shareholders of six mutual funds (the “LifeTime Funds”). Their allegation was that the LifeTime Funds’ investment advisors, Defendants Principal Management Corporation (“PMC”) and Principal Global Investors, LLC (“PGI”) (collectively, “Defendants”), breached their statutory fiduciary duty under Section 36(b) of the Investment Company Act of 1940 (“ICA”), 15 U.S.C. § 80a-35(b), by charging unfair and excessive fees for their advisory services and retaining excess profits derived from economies of scale. The Defendants immediately filed a motion to transfer the case to the Southern District of Iowa, which was granted.

The LifeTime Funds were diversified portfolios of Principal Funds, Inc. (“PFI”), an investment company headquartered in Des Moines, Iowa. The only holdings consisted of other PFI mutual funds (a so called “fund of funds”), and those holdings would change over time as the date of an investor’s expected retirement approaches (a “target-date” fund). The Investment Company Act of 1940 provides the following relief:

“…the investment adviser of a registered investment company shall be deemed to have a fiduciary duty with respect to the receipt of compensation for services, or of payments of a material nature, paid by such registered investment company, or by the security holders thereof, to such investment adviser or any affiliated person of such investment adviser. An action may be brought under this subsection by the Commission, or by a security holder of such registered investment company on behalf of such company, against such investment adviser, or any affiliated person of such investment adviser, or any other person enumerated in [15 U.S.C. § 80a-35(a)] who has a fiduciary duty concerning such compensation or payments, for breach of fiduciary duty in respect of such compensation or payments paid by such registered investment company or by the security holders thereof to such investment adviser or person.”

Principal Management Corporation and Principal Global Investors serve as the investment advisor and sub-advisor, respectively, of the LifeTime Funds. PMC provides extensive services to the LifeTime Funds, including monitoring PGI in its role as sub-advisor, providing portfolio management services, and providing substantial accounting, regulatory, compliance, and transfer agency services. PGI provides portfolio management services to the LifeTime Funds.

Every year, PMC and PGI make a proposal to the Principal Funds, Inc. Board of Directors (the “Board”) regarding the fees they intend to charge the LifeTime Funds. After considering and evaluating the proposal, the Board makes a final decision about the proposed fees at its September Board meeting in Des Moines, Iowa. The Board approves the fees, Defendants enter into contracts with PFI that govern the terms of Defendants’ relationship with the LifeTime Funds and set forth the fees that Defendants can charge the LifeTime Funds. The fees charged were the basis for this lawsuit.

Principal LifeTime Target-Date Funds….

Principal LifeTime Target-Date Funds are offered as a publicly traded investment, and as of 1/31/2017, Morningstar Star Rating rated these funds overall as follows:

- Principal LifeTime 2010 Fund (A) (PENAX)….. 2 stars out of five total

- Principal LifeTime 2020 Fund (A) (PTBAX)….. 3 stars out of five total

- Principal LifeTime 2030 Fund (A) (PTCAX)….. 3 stars out of five total

- Principal LifeTime 2040 Fund (A) (PTDAX)….. 3 stars out of five total

- Principal LifeTime 2050 Fund (A) (PPEAX)….. 3 stars out of five total

- Principal LifeTime Strategic Income Fund (A) (PALTX)….. 2 stars out of five total

T. Rowe Price & Brown Target-Date Funds….

Compare the above funds to T. Rowe Price & Brown, another provider of Target-Date funds…. for the same time period.

- Target-Date 2010 (TRRAX)…. 5 stars out of five stars

- Target-Date 2020 (TRRBX)…. 5 stars out of five stars

- Target-Date 2030 (TRRCX)…. 5 stars out of five stars

- Target-Date 2040 (TRRDX)…. 5 stars out of five stars

- Target-Date 2050 (TRRMX)….5 stars out of five stars

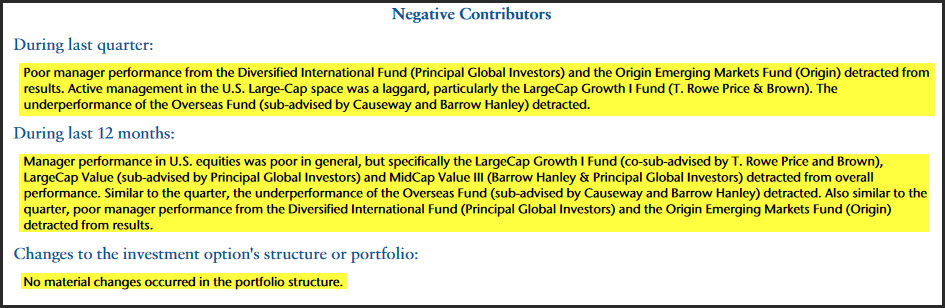

The T. Rowe Price Morningside performance rating is definitely higher. Yet, the T. Rowe Price co-advisor performance with Principal was “laggard” for the same time period, as is stated in the commentary highlighted below. If you find the portal for the above Principal funds on the Principal Website, you will find identical “negative contributors” commentaries for all of the funds…. illustrated below…

Principal Lifetime Target Date Funds under-perform many of the other target date fund options available, before any consideration of fees. The above commentary clearly illustrates the fact that “management performance” is lacking, but even worse, the funds are loaded with sub-advisors and “co-sub-advisers.” Each advisor, sub-advisor, and co-sub-advisor charges Principal a fee that you, the investor will pay… eventually. In this case, Principal Management Corporation is the advisor (Fee #1), and Principal Global Advisor is the sub-advisor (Fee #2). Then, as PGI sees fit, they will hire sub-advisors, which in the above commentary, includes T. Rowe Price and Brown (Fee #4), Causeway and Barrow Hanley (Fee #5).

The list goes on… the following image shows “other” subsidiaries of Principal Global Investors, PGI being an “asset management affiliate” of the Principal Financial Group…

I have no clue exactly how many “majority owned” affiliates of Principal International, Inc. actually exist, but the list continues to grow. Keep in mind that Principal Management is also an “advisor” to Principal Funds, and oversee Principal Life Insurance Company’s “proprietary due diligence process”…

But exactly what is the investor getting for his money. The above documents show that Principal’s management performance was lacking when compared to other Target-Date fund providers.

Principal LifeTime Target-Date Funds and excessive fees…

American Chemicals & Equipment, Inc. 401(k) Retirement Plan filed a lawsuit against Principal Management Corporation and Principal Global Investors, llc, asking for $300 million in damages. Their retirement investors had invested in the six LifeTime Target Date funds offered by Principal, suspected to be institutional shares, since the fees billed to the Plan by Principal included those fees charges against the Plan for advisors, sub-advisors, and co-sub-advisors. Institutional class shares typically have minimum investment levels of $5 million, $10 million or even higher. Even if you can invest $5 million, the fund company will probably not sell you the shares unless your are actually an institutional financial company. The institutional shares of some mutual funds can be invested in through wrap accounts offered by financial planners or investment advisors. Of course, the advisors will tack their own fees on top, negating the benefits of buying low expense institutional class shares.

Buying institutional class shares of any mutual fund can be compared to buying a cup of coffee. You can walk into Starbucks and for 5 bucks, buy a cup of coffee. Likewise, a savvy investor can purchase public shares of Target-Date mutual funds on the open market.

Your second option is to ask Starbucks to go down to their local Walmart, buy a coffee maker, some filters, a bag of Starbucks coffee, and coffee cup, and and brew a cup of coffee. Starbucks can then legally bill you for the total cost of producing that cup of coffee. Likewise, when you ask Principal to sell you an “institutional share” of their publicly traded Target-Date Fund, they will include charges for the “production” costs, aka advisory fees. These fees cannot be negated as disclosure is required by the SEC.

In addition to the excessive fee issue, you are now purchasing “proprietary funds” owned by Principal, and they are selling to you in a private sale. If you still do not understand the relationship, since Principal is likely the “plan provider,” acting on behalf of the plan participants, aka the employees, you are effectively purchasing this product at whatever price Principal decides to sell it to your Plan. And remember the advisors, etal? they are mostly subsidiaries and/or affiliates of Principal, so when the Board of Directors at Principal Management decides to accept the quoted pricing from Principal Global Investors, they are effectively self-dealing with their own company for advisory services.

American Chemicals & Equipment, Inc.(ACE) 401(k) Retirement Plan v. Principal Management Corporation and Principal Global Investors, llc

Ok, back to the lawsuit…. ACE sues Principal for $300 million in excessive fees. Principal has the case deferred to the U.S. District Court for the Southern District of Iowa, then files a motion to dismiss the case. The court refuses to dismiss the case based upon ACE’s standing to assert a claim…

“The Court finds that the Plaintiff has appropriately limited its claim to only those fees collected from Principal Fund interest holders and retained by Principal Fund advisers. Any dispute as to the work performed in exchange for this fee is a factual dispute not before the Court. As this is a fee assessed to Plaintiff as a security holder of the Principal Funds and they have brought this claim only on behalf of the funds in which they have an established interest, Plaintiff has statutory standing to bring this claim.”

On September 10, 2014, Judge John Jarvey ordered that the Defendant’s motion to dismiss, is in part denied. The case will be heard.

Sixteen months later, on February 3rd, 2016, Judge Jarvey files an Order, dismissing the case on a “standing issue.” On November 16, 2015, Principal defendants had filed a motion for summary judgment…“The Court previously ruled on Defendants’ motion to dismiss, in which it discussed a standing issue which has proven to be the heart of this case. In its motion for summary judgment, Defendants reiterate their standing arguments in addition to arguing that Plaintiff has failed to raise a genuine issue of material fact with respect to the merits of its ICA claim.”