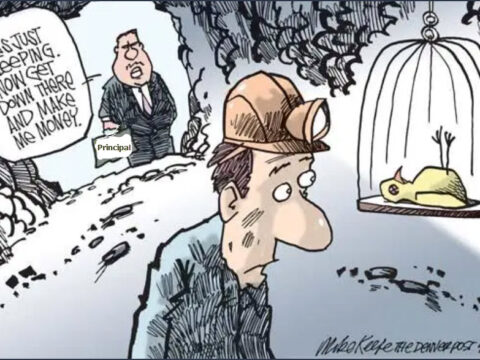

Posted in Regulations Protected: The Principal Group of Companies are ignoring Iowa regulations… Dennis Myhre This content is password protected. To view it please enter your password below: Password: Author: Dennis MyhreMr. Myhre can be contacted at..... dmyhre@fiduciaryfactor.com Related Articles Protected: 401k Savings Slashed in 2022! Protected: Pooled Separate Accounts… understanding your 401k Protected: “Just the Facts” about your 401k…. Protected: The truth about ERISA regulation…. continued