When you read published accounts of SEC causes of actions against companies like Wells Fargo Bank, you should assume they are guilty of those infractions, even though they may not be required to admit to their so-called “misconduct.”

While reporting on these actions, the SEC will often “soft sell” the misconduct, and, in the case of Wells Fargo, the SEC described the event as follows:

“Wells Fargo representatives involved did not reasonably investigate or understand the significant costs…” and “it is important that brokers do their homework before they recommend that their retail customers buy or sell complex structured products”… that… “came with high fees and commissions.”

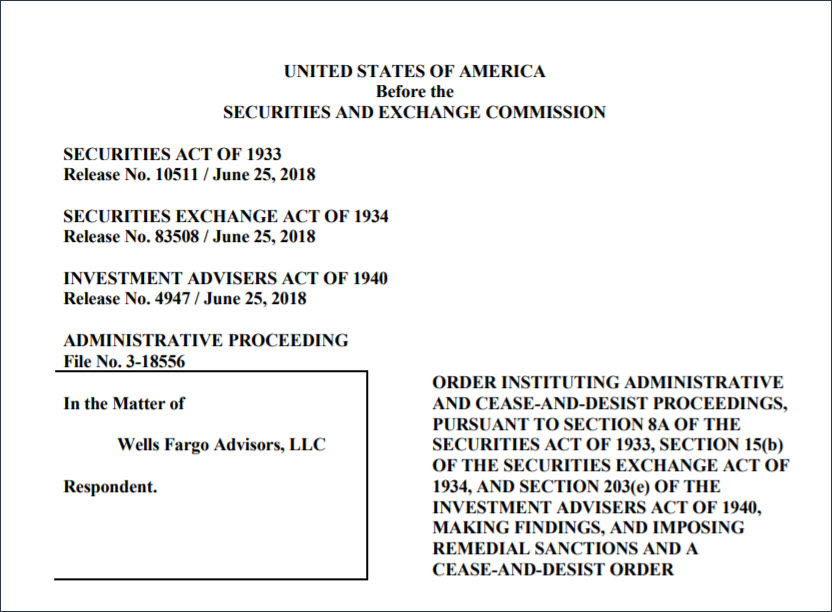

SEC cease and desist order to Wells Fargo Bank

If you review the “Cease and Desist” Order located at the above link, the “summary” describes the crime for which Wells Fargo was being sanctioned:

“From at least January 2009 through June 2013, certain registered representatives at Wells Fargo Advisors, LLC (“WFA”) and its predecessor Wells Fargo Investments, LLC (“WFI”)2 improperly solicited customers to redeem their market-linked investments (“MLI”) early and purchase new MLIs without adequate analysis or consideration of the substantial costs associated with such transactions. “

“An MLI is a fixed maturity financial product whose interest is determined by the performance of a reference asset or market measure such as an equity or commodity index over the term of the product. MLIs have limited liquidity and significant upfront fees, and accordingly WFA considered them to be products intended to be held to maturity and in 2011 implemented a policy prohibiting representatives from engaging in “short-term trading” or “flipping” of MLIs. Notwithstanding WFA’s internal guidance and policy, and despite the adverse economic consequences to WFA customers, certain WFA representatives did not reasonably investigate or understand the significant costs of MLI exchanges. Nevertheless, they recommended to their customers that they redeem their MLIs early, typically to realize profits, and to use the proceeds from those redemptions to purchase new MLIs. Supervisors routinely approved the recommendations or the exchanges. This practice caused certain WFA customers to incur significant costs and impaired the customers’ ability to achieve their investment objectives. As a consequence, WFA obtained commissions by means of recommendations that contained implied representations that WFA personnel had formed a reasonable basis for the recommendations when they had not, in fact, done so.”

It appears the SEC would like us to believe that this activity was simply an accidental “error” on the part of Wells Fargo, and the cease and desist order will remind Wells Fargo advisors to not make this same mistake again.

Considering the facts that what Wells Fargo did was criminal under the law, and involved the stealing of retirement income from an unknown number of retirees, we should be offended by the action taken by the Securities and Exchange Commission. the SEC is protecting the wrongdoer, and are certainly not protecting your best interest, as they allege in their website:

How does it happen that working class Americans set aside trillions of dollars to save for retirement, only to become victims of corrupt companies like Wells Fargo and other corrupted companies?

In the case of Wells Fargo, they had “self-reported” the incident under a program offered by the SEC . This so-called “self-reporting” of criminal activity by investment advisers includes an “eligibility” function requiring the wrongdoer “cease-and-desist” the criminal activity and the settlement will include “disgorgement” of their “ill-gotten gains.”

No admission of wrongdoing is required, and it is business as usual for the advisor. The message our government regulators are sending to the parties they regulate is we will not regulate your crimes, and if you own up to your mistakes, we will protect you from prosecution, and leave the door open for you to continue your crime spree. In fact, the penalties reflect the real goal of the SEC… Wells Fargo pays the feds a healthy sum of money for their crimes:

” Respondent shall pay disgorgement of $930,377, which represents the commissions WFA earned on Representative A’s and Representative B’s Recurrent MLI Exchanges between January 1, 2009 and August 31, 2012, prejudgment interest thereon of $178,064.27, and a civil money penalty in the amount of $4,000,000, consistent with the provisions of this Subsection C. “

Self-regulation has dominated the financial industry for decades. The National Association of Insurance Commissioners (NAIC) works closely with the insurance industry to write laws that supposedly regulate the industry, but the opposite is true. If you review the insurance laws in most states, you will find the regulations provide no protections for the 401k investor. In fact, most State regulations reduce the rights of retirement savers to that of a Class 2 investor.

The Iowa state laws, for example, require the insurance company ot “own” all plan assets, and The insurance company cannot be a Trustee. In the event of a foreclosure action against the insurance company, the rights of all investors are relegated to that of a Class 2 investor.

As an investor, your “best interest” will be taken seriously only when Federal regulators prosecute the wrongdoers in companies like Principal and Wells Fargo, and bring them to justice. Forget the Non-Prosecution Agreements, Deferred-Prosecution Agreements, and the SEC’s SCSD Initiative. Most importantly, rewrite the Federal Sentencing Guidelines and start prosecuting individuals and not the companies they work for.

A couple years ago, Principal Financial purchased Wells Fargo’s retirement accounts for $1.2 billion, which included over $700 billion in managed funds including 401k plans. Principal had their own problems involving the Securities and Exchange Commission (SEC), and were also ordered to “cease and desist” selling overpriced mutual fund classes at inflated fees.

Unfortunately, 7.5 million retirement investors had previously chosen to use Wells Fargo for their retirement savings option, and now, through an unprecedented purchase agreement, those same investors will be serviced by a corrupt and unethical insurance company. Added to the mix are the existing 7 million or so Principal clients, so now 15 million retirement savers will be managed by what is believed by many professional financial advisers as the most corrupt insurance company offering 401k plan services today.

For you, a Wells Fargo 401k Plan fiduciary or employee, this is the time for change within your company. You no longer have to confront your Wells Fargo advisor, and you owe nothing to Principal. Even though the Wells Fargo advisor will now be working for Principal, the evidence of wrongdoing by both companies in recent months provides you with a valid reason for change… so make the move.

As for Principal clients, the same facts exist… use the recent SEC “cease and desist” action by the SEC to warrant change for your employer to move your 401k to a plan provider with more integrity and higher moral values. If your Wells Fargo or Principal advisor claims they did not “admit” to any wrongdoing, suggest they not insult your intelligence and show them the door.